By Tim Leung, Ph.D.

In the US market, institutional investors own or manage a major share of public equities. For many institutional investors, orders to buy or sell stocks can be very large. Such orders are thought to be potentially costly to implement, as they create substantial immediate demand/supply and possible adverse price effects.

A large buy/sell order may cause other traders to raise/lower their offered price because they perceive a change in value from the contra orders of the institutional investor. This additional implementation cost due to short-term liquidity demand is often called market impact.

Practitioners commonly view this as a significant cost to track, avoid or minimize. This can be done by slowly trading the asset, which usually reduces market impact by minimally affecting demand/supply over time. However, this strategy exposes the agency trader to the risk in the stock price movement as well as the failure to complete the buying/selling of all desired units of stocks. Hence, it is the goal of many algorithmic traders to decide how to strategically trade off cost and risk for an institutional trade.

Optimal Trade Execution Problem

In our paper, we analyze a continuous-time stochastic model for optimal execution using both market and limit orders. Our article extends the foundational market impact model of Almgren & Chriss (2000) by including limit orders with uncertain fill rates, and a speed limiter that penalizes overly large trading rates. Unlike Almgren & Chriss (2000), our model has two order types, which can potentially have negative signs (i.e. submission of sell orders in a buy program or vice versa).

Additionally, we construct penalties that drive the optimal trading rates in the desired direction of complete liquidation. Specifically, we include a non-liquidation terminal penalty as well as a penalty, called trader director, to push trading rates for market and limit orders to be in the same direction. In combination, these three penalties (non-liquidation penalty, trade director, and speed limiter) force the algorithm to trade to full liquidation, while simultaneously tailoring the sign and magnitude of the trading rates. Finally, our model is capable of generating optimal strategies that very closely follow any given benchmark trading schedule while minimizing trading cost.

Our objective is to investigate how to optimally allocate aggressive (market) and passive (limit) orders over time to achieve trading goals. The aggressive nature of market orders tends to result in a higher market impact, whereas limit orders have less market impact but are less likely to fill. We model this fill uncertainty using an affine function of the trading rate in limit orders; this leads to an additional diffusion term that is correlated with the stock price process. The optimal liquidation problem is then cast as a stochastic optimal control problem, whose associated nonlinear Hamilton-Jacobi-Bellman (HJB) equation can be simplified to a system of linear ordinary differential equations (ODEs).

We then explore the special cases of constant and linear uncertainty to examine the properties of the solutions and analyze the corresponding explicit optimal strategies. Among our results, we characterize the trader’s buy-sell boundary, which is a time deterministic function governing when order types are non-negative.

We also consider an alternative model to incorporate a benchmark trading schedule and show that our model is capable of generating optimal strategies that very closely follow any given schedule while minimizing trading cost. This allows us to understand a tradeoff between following schedule and seeking profits, and thus, evaluate how profitable it may be to deviate from schedule. Throughout the paper, we provide numerical results to illustrate the optimal liquidation strategies in various settings.

Among our findings, we derive the trading rates explicitly and further examine the conditions under which they are non-negative over the trading horizon. In addition, we also introduce the critical time span for an order placement program. If the trading horizon exceeds this critical time, the trader has too much time to explore profitable opportunities in trading the stock. This leads to an interesting and intuitive trade-off: the non-liquidation penalty must be increased in order to prevent the trader from using time to explore unbounded profit, resulting in over-trading.

In the final section of this article, we provide numerical results to illustrate the optimal liquidation strategies in various settings.

Stochastic Model & Features

Throughout, we adopt the perspective of a sell program. The mathematics for a buy program is completely analogous. Trading takes place over a finite trading horizon [0,T]. The trader selects two stochastic controls: (i) the trading rate of market orders, v(t), and (ii) the trading rate of limit orders, L(t), over time t ∈[0,T].

The trader’s stock holdings, denoted by x(t) at time t, are depleted by the trading rates, v(t) and L(t). To capture the uncertainty of limit order fills, there is an additional diffusion term that models the volatility in the trader’s position due to limit orders.

In addition to incorporating permanent and temporary price impact of trades, our model also addresses an adverse selection effect that is often considered in algorithmic trading models. Adverse selection is an implicit cost incurred when, for example, the stock price rises just after making a sale. It would have been better for the trader to wait for the price rise before selling the stock, because then they would have realized an extra profit. For the model to incorporate an adverse selection effect, we want the trader to make an excess sale in limit orders. Our model includes a parameter setting that satisfies this adverse selection criterion, though our model also works when it does not hold.

We next incorporate four model features: (i) quadratic terminal penalty, (ii) trade director, (iii) trade speed limiter and (iv) scheduling penalty. The first penalty is added so trading will push the position towards liquidation. To achieve this, we add a quadratic penalty so that incomplete liquidation is undesirable. The second penalty is introduced to penalize placing buy-side market orders and sell-side limit orders (or vice versa) simultaneously. With such order placement, it would be as if the trader were buying/selling the stock between him/herself. This penalty is called the trade director. The goal is to encourage orders to have the same sign. In combination with the non-liquidation penalty, we expect that only the choice v(t)≥0, L(t)≥0 (rather than any other sign choice) will be desirable.

We also add a speed limiter to prevent the trader from trading too quickly with either order type. In other words, we allow the management to set two trading speed caps (upper and lower bounds) for market and limit orders.

For the final penalty, suppose the trader is given a time-deterministic schedule function, Q(t), to follow as closely as possible for all times t ∈[0,T]. In order to keep position x(t) close to Q(t), we consider a time-dependent penalty integrated over time, where the weighting function allows us to penalize deviations non-uniformly in time. This penalty is added to the trader’s P&L.

The trader’s objective is to maximize the expectation of the compensated P&L by choosing trading rates for market and limit orders. This amounts to solving a constrained stochastic control problem. This leads us to study the associated HJB partial differential equation (PDE) problem. An analytic solution to the stochastic control problem is derived in the paper.

Numerical Examples

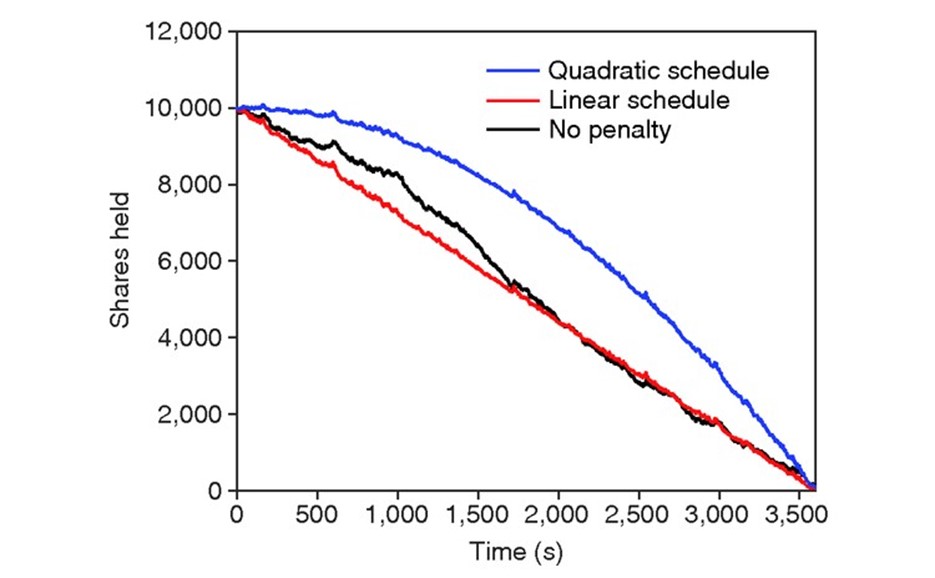

As shown in Fig. 1, the trader’s position persistently tracks the schedule over the trading horizon given a small penalization for deviation. Compared to the linear schedule, the quadratic schedule is useful for an institution that seeks to start out trading slowly and eventually speed up at the end of the sell program. We see that our model is capable of handling complicated non-linear schedules for stock holdings over time.

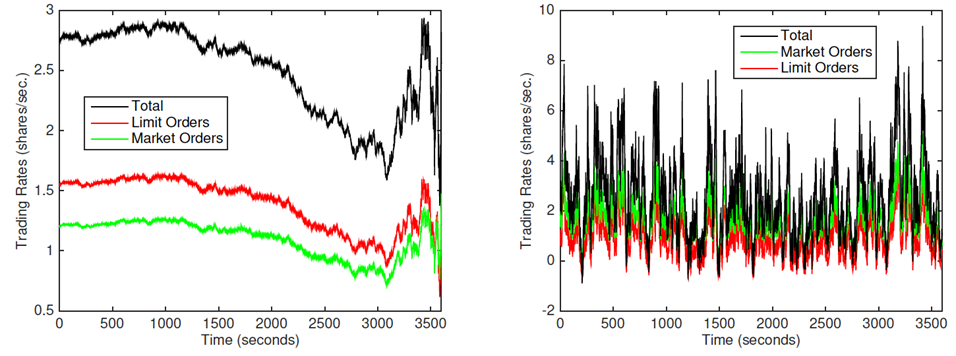

We examine the effects on trading rates in the next figure. On the left panel, there is no penalty for deviating from the linear schedule, while on the right we give a small penalty for deviating. We find that the penalized allocator trades much more quickly and reacts more quickly to price movements. Indeed, the non-penalized trading rates are very stable until the very end of the sell program and the penalized trading rates change rapidly over time. In contrast, the total trading rate in the non-penalized case (right panel) is fluctuating in a relatively small range. In the penalized case, more market orders are used over time, but the opposite is true when the penalty is removed.

By incorporating a number of new features, our order placement model allows for better control of the trading problem. For example, the trade limiter and director regulate the speed and direction of trades. Moreover, the multiple penalties lead to a number of trade-offs. Among them, we find that the trade director cannot be too strong or too weak unless the speed limiters are sufficiently severe.

The literature on optimal execution continues to grow in volume and diversity. One direction for future research as pertained to our order placement problem is to expand the trading platform to include multiple exchanges to allocate orders. These exchanges have varying costs of filling orders and risks associated with them. This gives rise to a venue allocation problem. Another related problem is trading in lit and dark pools. Whereas in a lit pool (or exchange) the order book imbalance can be observed, a dark pool blinds the trader from such information. This suggests a robust optimization or model uncertainty approach to optimal execution not previously considered. Furthermore, the problem of optimal liquidation is applicable not only to stocks, but also to options and other derivatives.

References

B. Bulthuis, J. Concha, T. Leung and B. Ward, Optimal Execution of Limit and Market Orders with Trade Director, Speed Limiter, and Fill Uncertainty [pdf], International Journal of Financial Engineering, Vol. 4, issue 2, p.1750020, 2017

Fast & Precautious: Order Controls for Trade Execution, RISK Magazine, April Issue [pdf] 2017

“New execution algos show complexity is not to be feared” RISK Magazine